** Lendy / Saving Stream review updated April 28th 2017 **

After 18+ months of lending, I still recommend Lendy / Saving Stream as they continue to revolutionise peer to peer property bridge loan and development investing. Lendy / Saving Stream allows you to invest in property developments without the need for millions of pounds in your bank account. Bridging loans can be high risk so due diligence is recommended to select the good quality loans.

My April 2017 Allocation: Slightly Increased

My annual rate of return: 11.75% (Net return after bad debt and fees but before tax)

* This opinion risk grade factors in types of loans offered, interest rates, platform history, default numbers and my own investing experience.

The Lendy / Saving Stream Review – What You Need To Know:

Pros

- Up to 1% return paid to lenders monthly

- All loans secured by property

- Reasonable default rates

- Loan status is now clearly displayed

- Lendy / Saving Stream collects entire loan interest from borrower

- Lender pre-funding available for all new loans

- Provision fund

- Secondary market for lenders to buy and sell loans

- Easy to use

Cons

- Property bridging development loans at high interest rates can be risky

- Increasing number of loans are past their end date

- Lender demand is higher than borrower supply

- Some loans pay lower returns

- Due diligence / time is needed to pick the good loans

- All eggs in property basket

- Need funds in account to purchase secondary market loans (effective early March 2017)

- High demand & Captcha makes secondary market difficult to use for buying

- Website can become unresponsive when user traffic is heavy

Lendy / Saving Stream is one of the most popular peer to peer lending sites despite being in the higher risk category.

The Lendy / Saving Stream website is easy to use and the competitive secondary market remains active, especially after new loan releases. The instant deposit feature means no wait investing and the pre-funding option saves you having to screen watch to catch new loans.

Lendy / Saving Stream: My experiences so far….

I have been investing in Lendy / Saving Stream since early 2015 and my experiences have mostly been positive. I’ve been able to invest in a variety of loans all paying 1% per month returns and interest payments have always been on time. I always use the pre-funding option for new loans and have some success buying on the secondary market. The secondary market rules now reuqire lenders’ to have fund intheir account to buy loans so selling some loans can take several days. I always try sell the oldest loans and reinvest in newer ones because selling older loans reduce risk. There are a few loans a hold to term if I’m confident in the borrower and security.

Recently I’ve noticed quite a few loans are in the past due period. I reached out to a Lendy / Saving Stream representative and here was his response:

“Over recent weeks there has been a small increase in the loans that are overdue. This is however not unusual given the nature and complexity of the loan book. We are actively supporting each borrower, either to arrange a refinance, repayment or extension for these loans. In the event that we became concerned about any of these loans we would move to default the borrower. In most cases it is just that the borrower is experiencing delays in refinancing or the sale of the property.”

I agree with the response and while it’s better for all loans to be completed on the due date, sometimes this just isn’t realistic due to the nature of property development.

What Is A Lendy / Saving Stream?

Lendy / Saving Stream is a peer to peer lending company that offers secured property bridging and development loans. A bridging loan is a short term loan given t a property developer while they attempt refinance. Lendy’s loans are given to borrower at rates up to 1.5% per month. Bridging loans are common in the real estate investment world. In the event of a loan default, Savings Stream attempts to sell the security in order to cover lenders capital and interest.

Sometimes Lendy converts bridging loans into development loans to allow to borrowers to move forward with construction.

When Did Lendy / Saving Stream Launch?

January 2013

How Do I Sign Up?

Easy! Click Here. (I receive 1% of your initial investment as a referral payment. This payment is made by Lendy / Saving Stream and does not come from your investment. When you open an account through my website it helps me to continue to operate and offer this reviews.)

What’s The Signup Process Like?

Painless. They run the usual i.d. checks, no additional identification needed.

Are They Regulated?

Yes, by the UK Government’s Financial Conduct Authority under Interim Permission.

What’s The Minimum Deposit / Investment?

Deposit: Minimum £100 via bank transfer for your first deposit

Loans: £100 minimum for pre-funding on new loans and £1 minimum on secondary market loans

How Much Interest Does Lendy / Saving Stream Pay Lenders?

Up to 1% per month

Is Interest Paid Immediately Or When the Loan Starts?

As soon as your investment goes live, interest starts to accrue.

When Is Interest Paid?

First of each month

What Are The Fees?

None to the lenders

How Much Time Is Needed Managing My Account and Investments?

Because bridging and development loans are high risk, more time is required to perform due diligence on the loans. Some lenders’ spend very little time researching these loans and prefer to diversify across as many loans as they can buy. This used to be my strategy when the secondary market was liquid but now, I buy loans planning on holding them to term in case I can’t resell them so more research time is required.

I recommend the due diligence route on loans before investing because it only takes one mistake to learn a painful default lesson.

How Long Are The Loans?

3-12 months but loans are often extended or can be paid off early.

What Security Does Lendy / Saving Stream Loan Against?

All loans are secured against property or land. Lendy / Saving Stream used to loan against boats and other items but they veered away from these types of loans. The loan-to-value ratios of the securities range from 11-70%.

What Are The Main Risks?

Company Failure: If Lendy / Saving Stream fails, investors could see losses although there are many unknown variables so no one knows how lenders would fare on the outcome. The new structure should reduce lenders risk but platform failure is always a concern as it’s hard to predict.

High Borrower Rates / Lender Returns / Borrower Default: With high returns comes higher risk. Up to 12% annual returns to investors mean the borrower is paying 1.5%+ monthly. However, this is standard in the property bridging loan business. High borrowing rates mean the loans can be high risk and the risk of default is always present. Lendy / Saving Stream recently starting offering lower interest return paying loans but I’m not sure these loans are any less risky than the 12% paying loans.

Valuation Errors: If Lendy / Saving Stream or it’s vendors over-value a piece of property and the borrower defaults, investors may lose money if the property sells for less than the loan balance.

Underwriting Standards: If Lendy / Saving Stream loosens its credit standards, defaults could rise substantially. Lenders place great amounts of trust in Lendy / Saving Stream’s ability to provide lenders with quality loans. No problems have surfaced so far but it is something I continually watch for.

Property Market Downturn: The recent Brexit triggered a secondary market loan glut as lenders became nervous about possible declines in property values. Lendy / Saving Stream even suspended and cancelled upcoming loans. This event highlighted how a single economic event can affect peer to peer lending. If the market downturns, property values could decrease and a defaulted property sale could recoup less than the loan amount and expenses; resulting in lender losses.

Sector Specific: Being heavy in the real estate sector is risky should a downturn occur. Defaults could increase and property values could fall.

Is There A Provision Fund?

Yes. The fund aims to hold a balance equal to 2% of the entire Lendy / Saving Stream loan book total.

Am I Lending To Lendy / Saving Stream Or To Borrowers?

In the olden days, ok 2015, lenders were lending to Lendy / Saving Stream (or Lendy Ltd). In 2016 Lendy / Saving Stream announced they were changing their legal structure to better protect lenders. All new loans are ring-fenced and some of the older loans are too (when Lendy / Saving Stream deems it necessary). This means investors are lending directly to borrowers rather than to Lendy / Saving Stream; good news for lenders.

What Happens If Lendy / Saving Stream Goes Bust?

The consequences of a failure would likely be devastating because there is no way to know if investors would be able to recoup their money. Direct from Lendy / Saving Stream’s website:

“If our platform were to fail or we and/or Lendy / Saving Stream Security Holding become insolvent we would transfer our obligations under the Terms and the Loan Contract to a third party back up servicer, with whom we have entered into a back up servicing arrangement.”

Not much information to go on here so always remember that if Lendy / Saving Stream fails, your money is at risk so don’t invest more than you are comfortable losing.

WHAT I LIKE ABOUT LENDY / SAVING STREAM:

High Paying Lender Returns

In the era of ultra low-interest rates, 12% annual returns are attractive. Interest payments are made on the first of the month and can usually be reinvested in secondary market loans. All my payments have been received on time, every time.

New Loan Prefunding

As more lenders joined Lendy / Saving Stream, demand outstripped supply and loans became harder to buy. This meant that not only did you need to be logged in at the exact time of a new loan being posted, but you needed some fast fingers. Some of the smaller loans would be sold in seconds with larger loans filling in just a few minutes.

Lendy / Saving Stream combated the endless lender grumbles by introducing pre-funding on new loans. Pre-funding of new loans doesn’t require you to have the money in your account. After you receive your loan allocation, you must pay Lendy / Saving Stream within 24 hours or they will release your allocation. This innovation bypasses one of the biggest inconveniences lenders have to suffer on most peer to peer lending platforms: the dreaded bank to platform deposit wait.

One thing to note is if you use the platform credit to buy newly issued loan pieces, you cannot sell those loan pieces for seven days if you used the credit feature. This is to prevent people from gaming the system and buying more than they need.

Here is how to set your pre-funding request from the Loans page:

Loan allocation always depends on demand and supply so you never quite know how much your assigned amount will be. Based on my own experiences, here’s what I’ve received:

You can see that for larger loans, you will generally be assigned your total pre-funding request but this could change as more investors come on board.

Savings Stream uses a bottom-up pre-funding system for loans under £1m, where the smaller sum investors are allocated their pre-funding amounts before larger investors.

NEW: Loan Status Clearly Displayed

Recently a column was added to the loan table which shows a loans status. This feature is a welcome one for lenders who want Lendy / Saving Stream to be more transparent.

Here is what the abbreviations mean (You can also hover over the ? symbol for an explanation.):

IOA: Interest On Account

This is interest paid upfront by the borrower to service the loans monthly interest. This means the loan is in good standing.

SBL: Serviced By Lendy

Lendy (aka Lendy / Saving Stream) covers the monthly interest while loan repayment or restructuring is negotiated.

IA: Interest Accruing

Interest accrues as a credit on lenders account but is not paid until it is recovered from the borrower through the disposal of the security. This means the loan is either in negotiation to be closed or on its way to defaulting.

DEF: Defaulted

Self explanatory and a loan you don’t want to be invested in.

Secondary Market

Lendy / Saving Stream’s secondary market is very easy to use and used to be relatively liquid for selling. Demand and supply has heavy impacts on the way the secondary market behaves. Post Brexit there was a glut of loans for sale but that phase quickly passed and in December 2016, there was barely anything for sale.

The secondary market has experienced a major slowdown since Lendy / Saving Stream now requires lenders to have the funds in their accounts to buy secondary market loans. Since bank transfer deposits can take time, a loan piece may no longer be for sale when your Lendy / Saving Stream account is credited. Lendy / Saving Stream is attempting to combat this slowdown by introducing a faster deposit system but I’m not convinced this will solve the secondary market problem. For now, I only buy loans I’m willing to hold it to the end. Previously, secondary market loans could be bought on good faith credit so the market was very liquid. One solution is to simply keep money in your account which many lenders aren’t used to doing.

You can sell any amounts of your loan pieces for free. I’ve found that if I put something up for sale that is in demand, it usually sells quickly. Loans with high queue amounts (see below) can take a few days to sell.

In the past, many lenders bought more loans than they intended to keep and sold their unwanted parts on the secondary market when newer loans became available. Lendy / Saving Stream has addressed this problem with rules preventing lenders from buying more of a loan than they intend to keep. If a lender uses account credit to obtain new loans and doesn’t have enough money in his account to pay for the new loan pieces, the lender cannot sell any of the new loan parts for seven days. If a lender has enough money in their account to buy the new loan allocations without using the credit system, this seven day limitation doesn’t apply.

This rule prevents lenders from requesting larger pre-funding amounts of new loans with the intent on selling existing loans to pay for the new loan parts.

Back to the secondary market. You can sell all of your loan or just a portion. Once you place a loan for sale, it is immediately available to other other lenders:

{kind=link}

The capital and interest in paid into your account as soon as your loan piece is sold. Simple.

This secondary market has been working well but beware, if a property downturn or recession occurred, a mass exodus of investors could make loan exit impossible.

One downside to the secondary market is when you place a loan part for sale, you immediately stop receiving interest. This isn’t usually a problem unless there is an oversupply of that loan but I think it’s better not to receive interest for a few days than to be stuck with a bad loan.

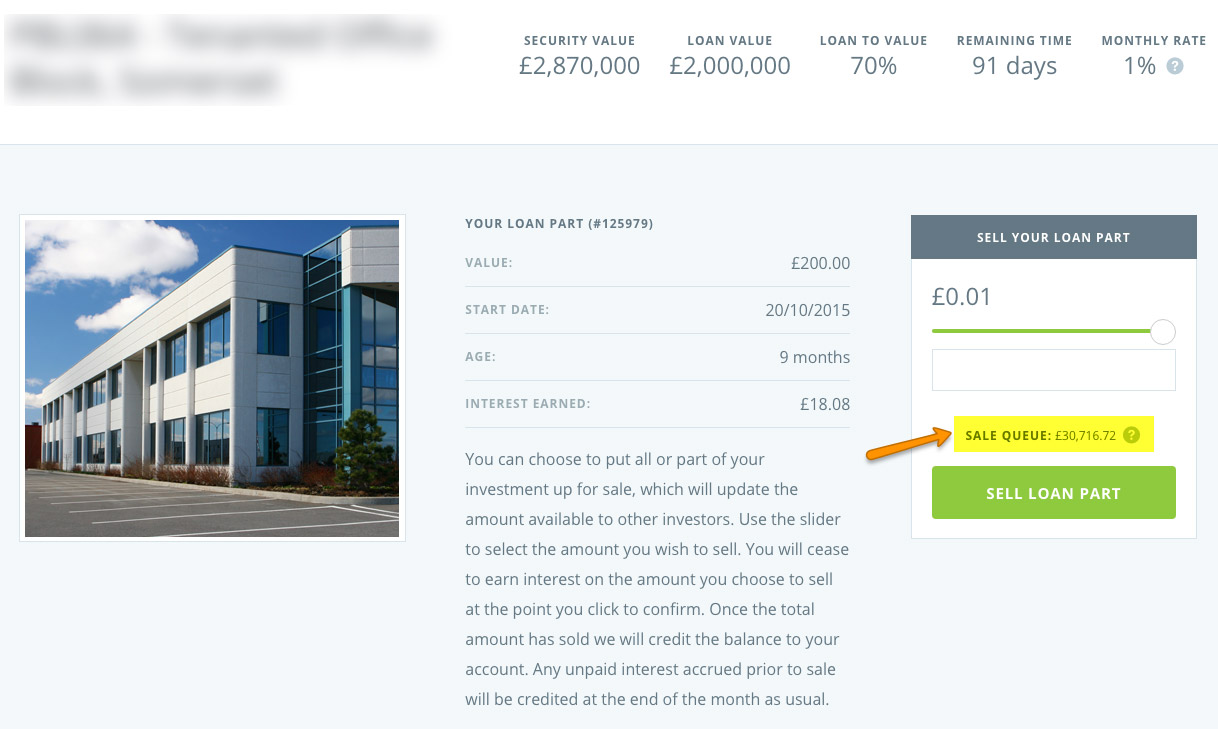

An excellent feature Lendy / Saving Stream recently added is when you click to sell a loan part, there is loan queue amount displayed so you know how much is for sale before your parts will be sold:

This feature allows you to decided whether to sell your loan pieces or wait until the queue has decreased.

For buying, high demand times can make the secondary market unforgiving. Loan pieces can sell within seconds plus there is a Captcha that sometimes appears preventing quick buying. Some people believe loan pieces are snapped up by automated purchasing bots. I’m not convinced.

Loan Security

All loans are secured by property at loan-to-values under 70%. In the event of a loan default, the security could be repossessed and hopefully sold to recover losses. While having security is good, it’s important to understand which security is good and which is questionable. For example selling a farm or land can be more difficult than selling a house. Also, the lower loan to value deals are better if the valuations are accurate.

Entire Loan Term Interest Payments Are Collected Upfront

This is a major plus. For example, if a loan is given to a borrower for 12 months and the interest payments are £10,000 per month, £120,000 is collected from the borrower in advance. This ensures lenders can be paid for the full 12 months. It’s an extra level of security that I really like.

The Provision Fund

Provision funds always offer an extra layer of protection against borrower defaults. In theory, this discretionary fund could be used to compensate lenders should a shortfall exist after a security sale. Currently, the fund stands at just over £3 million (January 2017). That will buy a few packets of Monster Munch!

Payments & Withdrawals

Interest payments are paid on the first of each month and have always been on time. Withdrawals are timely, usually landing in my bank account within 12-24 hours during business days.

The Website

The old website was great but was updated in December 2015. The new website has been improved but has experienced slowdowns and timeouts during high traffic times when new loans are released.

Loan Flow

Lendy / Saving Stream usually has a consistent flow of new loans. You can view the new loans using the pipeline tab.

WHAT I DISLIKE ABOUT LENDY / SAVING STREAM:

The Lower Paying Interest Rate Loans

Lendy / Saving Stream has started offering lower return paying loans in the 7 to 10% range. I’m not sure these loans are less risky than the loans that pay 12% so I tend not to invest in them unless I’m sure the security is good. I think the lower paying loans are an attempt to access new borrowers since loan supply has been struggling to keep up with lender demand. It’s possible these lower paying loans could be the new norm.

Secondary Market Changes

If I had a neutral section of likes and dislikes, the secondary market changes would go there as I both like and dislike them. The new changes went into effect in March 2017 and will no longer allow lenders to buy secondary market loans without having the money in their accounts. This is both good and bad.

The Good

These changes are good because it means Lendy / Saving Stream are complying with the FCA regulators who probably mandated this change in order for Lendy / Saving Stream to receive full authorisation. Also, the changes may reduce the competitiveness of the secondary market which has always been cutthroat. Lenders may not be so willing to have funds sitting in their account as they wait for other lenders to sell loans which will result in less buyers.

The Bad

The hassle factor of needing liquid funds in your account decreases the attractiveness of what was once a great secondary market. Also the liquidity of the market has slowed way down and sometimes loans can take time to sell. Gone are the good days when lenders’ could sell loans in minutes.

Sector Specific

Lendy / Saving Stream currently only offers real estate loans so if the property market goes down the spout, this could put a severe strain on its business model and lenders funds. It would have been interesting to see how Lendy / Saving Stream would have fared during 2007-2010 property decline. It’s important to diversify across different lending sectors so a downturn doesn’t hurt your returns too badly.

High Interest Rates For Borrowers = Higher Risk

Paying high interest returns to investors means Lendy / Saving Stream charges its borrowers up 1.5% per month. This increases the risk of default. This would be more of an issue if loans were for longer than 12 months but it’s still something to consider before investing.

Increasing Number Of Loans Are Past Term

I’ve noticed an increasing number of loans are past their loan term date. I’m not overly concerned at the moment but it is something I’m keeping a watchful eye on. It’s not unusual for property refinancing to take longer than anticipated so extensions are provided as needed. Hopefully, Lendy / Saving Stream remains transparent in its information.

Some of Lendy / Saving Stream’s loans are in the millions meaning that two or three defaults could really sting lenders. Currently, there is a £1.7m loan in default and it will interesting to see how this is recovered. It’s essential to diversify across many loans and not to be tempted to put too much money into any one loan.

Due Diligence And Research Time Is Needed To Identify The Good Loans

I highly recommend each loan valuation document and performing your own due diligence on loans. Researching the borrowers names and companies can uncover interesting information about past debt, bankruptcies and development experience. Unfortunately researching loans does take some time but it can help reduce your investment risks and is well worth the time.

The Website

During loan releases, the secondary market part of the website experiences severe slowdowns. Try to buy a loan part and the dreaded spinning ball can keep you guessing for minutes whether or not your purchase was successful. I’ve found that if my purchase was successful, my Available Funds amount will change instantly even though the page is still thinking. There is also a nasty Google Captcha verification that can rear its ugly head after two or three attempts at buying. This Captcha has made purchasing on the secondary market extremely difficult when demand is high.

My Strategy

When I first began investing in Lendy / Saving Stream, the secondary market was a beautiful feature since you were able to buy and sell loans very easily. Now the need to have funds in your account has slowed the secondary market demand. Post Brexit loan supply has highlighted the reality of how lenders may not be able to sell loan pieces during economic changes. With this in mind, I invest in loans I’m prepared to hold long term. Since the loan supply has reduced, it’s important not be tempted to over invest in any single loan. The key to Lendy / Saving Stream (and every peer to peer platform) is due diligence and diversification.

When possible, I sell loans that are within 45 days of ending unless I’m extremely confident in the security. I reinvest sold loan money into the newest loans. A fresh loan book means decreased default risk since loans term interest is collected in advance.

Conclusion

Lendy / Saving Stream is recommended for anyone looking to lend within the property sector. 12% bridging loans are high risk so expect defaults, especially during unstable economic times. Lendy / Saving Stream lessens risk by including a provision, securing loans with property and collecting loan repayments in advance.

The website is easy to use and there is a secondary market to buy and sell loans. The new loan pre-funding option saves you from having to constantly monitor the website to get a piece of the action.

Sign up for Lendy / Saving Stream peer to peer lending and start earning up to 12% annually. (I receive 1% of your initial investment as a referral payment. This payment is made by Lendy / Saving Stream and does not come from your investment. When you open an account through my website it helps me to continue to operate and offer this reviews.)

If you enjoyed my Lendy / Saving Stream review and want to learn more about peer to peer lending, click here and receive my complimentary Top 5 Peer to Peer Lending Sites Report.

I love feedback, so if you find any errors or omissions or have any improvement suggestions, I invite you to contact me and be a part of contributing to this website.

** This unbiased Lendy / Saving Stream review is for information purposes only and should not be considered investment advice. Opinions expressed in this Lendy / Saving Stream review are based upon my investing experiences. All information was deemed to be correct at the time of writing. Peer to peer lending contains risks so never invest more than you can afford to lose. **